Endless Distractions

Endless Distractions

The key to a good magician performing sleight of hand is to distract his audience so they don’t see the trick being performed. Our enemies have perfected this trickery, constantly providing distractions to keep us chasing one thing after another while they are doing something far worse we don’t notice. Most of our political theater falls into this category. Normies get caught up in one political squabble after another over this issue or that, while at the same time behind the scenes They were stuffing our country with non-White migrants, legal and illegal, that reliably will vote to loot heritage Americans. In other words, while we are fighting mostly meaningless battles over tax rates and transvestites on beer cans, They were dealing our country a demographic kill-shot.

A great example of this hit the news last week, quietly at first but it is gaining traction.

One of the hottest of buttons in contemporary political discourse is the ludicrous issue of “reparations”, the paying of money to people that were never enslaved, paid for by people that never owned slaves. It has expanded now to include “historic injustices” that allegedly held black people back from being successful in America, rather than their own poor financial discipline and work ethic. Even in places like San Francisco where slavery was never legal, the city is having serious conversations about giving lump sums of money to black residents to the tune of millions of dollars. Jared Taylor just did a video about this….

With a straight face They tell us through their dimwit mouthpieces that even $5 million isn’t enough money to offset all of the “harm” suffered by blacks. Sure that sum would bankrupt already teetering San Francisco but isn’t that worth it to resolve an injustice?

What is amusing is that even after offering up a massive payout like $5 million per black, the panicked reparations advocates are saying it needs to be higher. How much higher is up in the air but the important thing is that whatever the figure proposed, they will say more is necessary. They will do this because the last thing “civil rights” types want is some sort of line in the sand because that would mean there is an end in sight and saying “Here is a check for X dollars, now STFU and quit bitching” would mean these black clergy, community activists and various other might have to find gainful employment. That can’t happen, so they instead focus on a concept rather than a figure.

Like I said, the number proposed is so ridiculous that even in loony San Fran it probably won’t happen, unless the city can start printing up their own money. That doesn’t mean it is useless, far from it. Those crazy numbers get the normies wound up and they don’t notice something else, something real….

Biden To Punish Good-Credit Homebuyers To Subsidize High-Risk Mortgages

From the article…..

A new rule from the Biden administration will force homebuyers with good credit scores to pay higher mortgage rates in order to subsidize loans to those with riskier borrowing profiles, the Washington Times reports.

The fee, which will apply to those buying or refinancing houses after May 1, will affect homebuyers with credit scores of 680 or higher, will amount to roughly $40 per month on a home loan of $400,000, or nearly $500 per year. Homebuyers who make down payments of 15% – 20% will be hit with the largest fees….

….Under the new Biden rules, those with lower credit scores and smaller down payments will qualify for better mortgage rates and discounted fees thanks to the surcharge on those with good scores.

It is impossible to overstate how much this turns the lending world on it’s head. The mortgage business is based on you promising to repay an enormous loan, typically many times what you make in a year, with the home for collateral. Contrary to the common belief, banks don’t want to foreclose on homes. It is a huge hassle and they usually lose money, not least because people who have a home in the foreclosure process often trash the place. To mitigate this, banks use your credit history to help guide their pricing. People who have historically been responsible with credit tend to continue to be responsible while those who have not been responsible with credit in the past tend to be poor credit risks. Not in every case of course but when looking at a huge portfolio of loans, past behavior is one of the best indicators of a future willingness to pay the loan back as agreed.

This model incentivized good behavior. Making your payments as scheduled, on time, meant a good credit score and favorable credit terms in the future in the form of lower fees and better interest rates. This is a net positive for society, we want people that borrow money to pay back that money. Doing so makes the system work (setting aside the arguments against usury which are completely irrelevant in our current situation). When people don’t pay back their loans, it causes a cascade of negative social impacts. As a society we want people to repay their loans and in return we incentivize them to do so. At least we used to.

Make no mistake, banks won’t take a hit on this deal. They are going to get insulated from the risk of bad loans in the form of higher rates and fees on good borrowers. The banks are never going to get hurt in these deals because the banks own the political class (see: Everyone Else Should Pay For My Poor Decision Making! for more on how the financial services industry owns both parties).

Under this rule, doing the proper and right thing, that is to say paying back the money you borrowed, is going to be punished and doing the wrong things, taking loans and not paying them back, will be rewarded. This will in turn drive up borrowing costs for the people most likely to repay loans and therefore push home ownership for everyone further out of reach. This is by design, more on that shortly.

As always the question is “Why?”. First let’s look at the cut-off point for being getting better rates and lower fees, from the Washington Times…

Mortgage industry specialists say homebuyers with credit scores of 680 or higher will pay, for example, about $40 per month more on a home loan of $400,000. Homebuyers who make down payments of 15% to 20% will get socked with the largest fees.

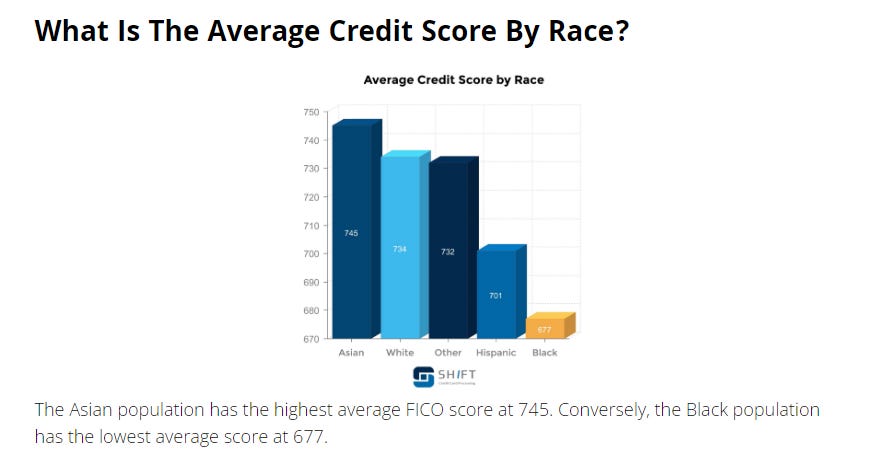

What is the point of choosing an arbitrary level of credit irresponsibility, in this case a FICO score of 680? Check out this chart from Shift on average credit scores by race….

If you are keeping score at home, you might notice that the average credit score chart looks an awful lot like an average IQ chart or average SAT/MCAT/GRE score chart: Asians at the top, Whites behind them, mestizos trailing quite a bit and then a huge drop-off when it comes to blacks. On the other hand, violent crime statistics when charted out are the exact inverse. Weird, almost like people with higher IQs tend to understand how to be responsible with credit and how to not commit crimes.

The average credit score for blacks is 677. The cut-off for getting favorable loan rates subsidized by people with good credit is 680. You might be seeing the picture at this point.

The answer to the question “Why” is two-fold.

First it takes from White and Asian borrowers who have spent a lifetime building their credit and gives to blacks who have spent a lifetime being irresponsible with credit. Or to put it another way, this is the latest backdoor reparations scheme. Whites and Asians with good credit will pay around $500 per year in higher interest and fees and those funds will be used to make it less expensive for blacks to get mortgages. You can only call that what it is, a direct transfer payment from Whites and Asians to blacks or more simply yet “reparations”. It is pure pandering, rewarding bad behavior from blacks with loot from Whites and Asians. On a standard 30 year mortgage, at around $500 per year in higher interest and fees, that works out to nearly $15,000 in extra expenses being shouldered by people who have tried to do the right thing.

The stated goal is “equity” and addressing “historic wrongs”, as if the only reason that blacks have such poor levels of home ownership and crappy credit is White people doing them wrong or getting an unfair advantage, and not because they are terrible with credit. As a personal example, my wife and I both come from intact two-parent families (formerly just called “families”). As a young married couple we had some real struggles with credit. Getting credit isn’t that hard, being responsible with it can be. It took us some time to dig out, a common problem (believe me, as a bank manager for years it is VERY common), but today we are sitting pretty with outstanding credit. Why? Did we get a special rate for Whites only? Could we draw from a pool of Whites-only cash to make payments if we were short? Nope. We did it the old fashioned way:

We paid back the debt we incurred at the agreed upon terms.

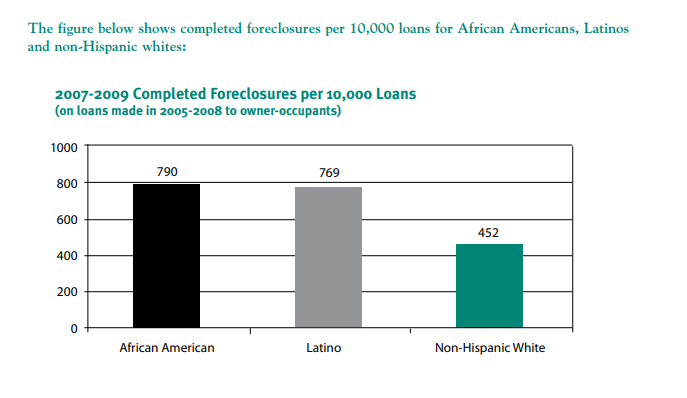

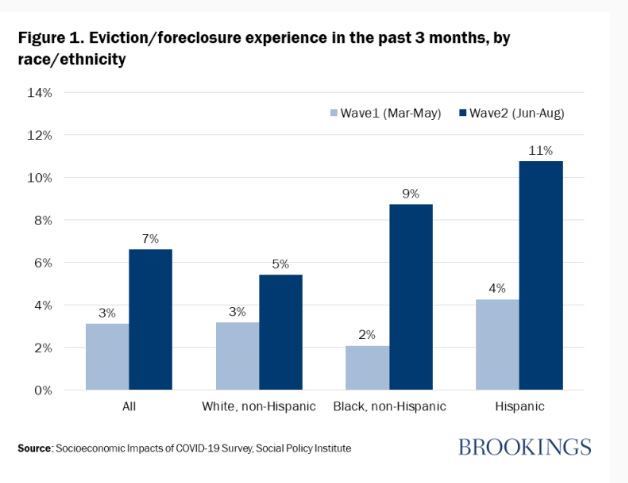

Meanwhile, while this is a little old and I didn’t feel like digging more, this is the rate of mortgage foreclosure by race:

I assumed this has not gotten better with time. I was correct. From The Brookings Institute in December of 2020 as the Covid response was causing catastrophe all around the country.

It brings to mind the issue of black graduation rates from college. Well meaning (?) efforts to push more blacks who were unprepared and unsuited into college has led to a huge number of blacks who a) put off learning a trade and gaining work experience for years and b) likely incurred a ton of student debt while c) not graduating. Only around 40% of blacks will complete a four year degree in six years (see: Participation Ribbon Egalitarianism Has No Place In Education). Likewise, pushing blacks who are not prepared and not suited to handle a mortgage payment every month in a 30 year commitment means more blacks getting in over their heads and then losing their home, destroying wealth and crippling their ability to get credit in the future.

It doesn’t help anyone. It doesn’t really help blacks, although they think it does, and it hurts Whites who are responsible with credit. So again I ask: why?

That brings me to the second point.

Making home ownership more expensive for everyone means an increasing percentage of the population that are renters.

Renting sucks. You throw money into rent every month and whether you rent for 3 months or 15 years, at the end you have nothing to show for it. No equity, no ownership. There is a reason that buying your own home was once called The American Dream. Now the American dream is seeing your mixed race adopted son getting castrated and declaring himself trans. It also puts you at the mercy of landlords.

In December of 2010 my wife and I signed our names over and over to documents that enabled us to buy our current home on four acres. We agreed to make a set monthly payment for a set number of months, and when we refinanced later on the terms changed slightly but the basics were the same. This payment every month by this date for this many years. Today, a little over a dozen years later, our house is conservatively worth double what we paid for it thanks to the explosive real estate market for places with acreage around here and the insatiable appetite for homes from the Amish. Our payment? It is still the same.

For renters in this market, the story is quite different. Rent has been rapidly rising, making it more difficult for people who already cannot buy a home (housing prices are also increasing rapidly) to rent a home. With higher prices, people are forced to rent smaller homes in worse neighborhoods. This also tends to make people less likely to have children as responsible people worry about being able to provide for offspring.

This is all intentional, something I keep bringing up. One of the key foundations of “The Great Reset” is that you will own nothing and be happy. People certainly are getting the first half of that in spades. See The Great Reset: A Solution In Search Of A Crisis for a more in-depth look at The Great Reset. Tucker had a decent video about this the other night and it includes a clip of some slimy weasel declaring that people really don’t want to own houses or cars.

While we are distracted by sportsball or DeSantis and Trump sniping at each other or a transvestite on a beer can, They are behind the scenes moving pieces around to accomplish their goals and that is precisely what this new rule is all about. Pushing the middle class down and away from the elites, forcing people to rent ever smaller homes and turning America into a feudal rental state run by Blackrock. The racial politics are just a bonus, the real reason is even more insidious.

Welcome to America 2023 where being a responsible person gets you punished and the values that made America great are under assault.